You can define a symbol to be a random variable and then query that random variable for information, or sample that random variable. There are many such continuous distributions programmed into Maple, but we will look at only a few that are relevant to engineering.

[> with( Statistics ):

This is a continuous distribution where there is an equal likelihood of a value appearing between two numbers $a < b$.

[> X1 := RandomVariable( 'Uniform( a, b )' ): [> Mean( X1 );

$\frac{a}{2} + \frac{b}{2}$

[> StandardDeviation( X1 );

$\frac{\sqrt{3} \sqrt{ (b - a)^2 } }{6}$

We can ask Maple for the probability density function and the cummulative distribution functions:

[> PDF( X1 );

$\left \{ \begin{matrix} 0 & x < a \\ \frac{1}{b - a} & x < b \\ 0 & \textit{otherwise} \end{matrix} \right .$

[> CDF( X1 );

$\left \{ \begin{matrix} 0 & x < a \\ \frac{x - a}{b - a} & x < b \\ 1 & \textit{otherwise} \end{matrix} \right .$

[> X1f := RandomVariable( 'Uniform( 1, 5 )' ): [> Mean( X1f );

$3$

[> StandardDeviation( X1f );

$\frac{2\sqrt{3}}{3}$

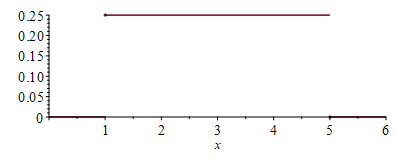

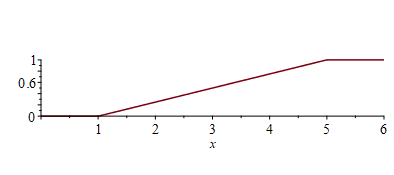

The probability density function is discontinuous, so we should use the 'discont' = true option:

[> plot( PDF( X1f, x ), x = 0..6, 'discont' = true );

[> plot( CDF( X1f, x ), x = 0..6, 'discont' = true );

[> f1 := Sample( X1f ): [> f1( 10 );

$[3.6203920158953626, 1.6504469407785223, 1.4759907262335066, 2.993456207928572,$ $4.838975834064325, 2.361542906664533, 3.3410710039191094, 1.895247757964548,$ $4.005068237222611, 2.0203804618370764]$

This is a continuous distribution equivalent to the usual bell curve with a given mean and standard deviation:

[> X2 := RandomVariable( 'Normal( mu, sigma )' ): [> Mean( X2 );

$\mu$

[> StandardDeviation( X2 );

$\sigma$

We can ask Maple for the probability density function and the cummulative distribution functions:

[> PDF( X2 );

$\frac{\sqrt{2}e^{-\frac{(x - \mu)^2}{2\sigma^2}}}{2\sqrt{\pi} \sigma}$

[> CDF( X2 );

$\frac{1}{2} + \frac{\textrm{erf} \left({\frac { \left( x-\mu \right) \sqrt {2} }{2 \sigma}}\right)}{2} $

[> X2f := RandomVariable( 'Normal( -2, 3 )' ): [> Mean( X2f );

$-2$

[> StandardDeviation( X2f );

$3$

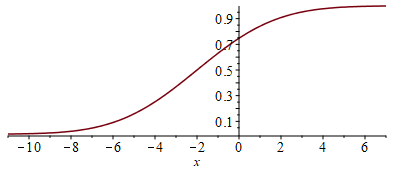

[> plot( PDF( X2f, x ), x = -11..7 );

[> plot( CDF( X2f, x ), x = -11..7 );

[> f2 := Sample( X2f ): [> f2( 10 );

$[1.2017008485503808, 2.2060565876883977, -4.162598640192476, -6.1174844206463295,$ $-0.35191374398380093, -2.0501804170515747, 1.8729911446438114, -1.2366724530815374,$ $-3.1180144880897274, -1.739101963430866]$

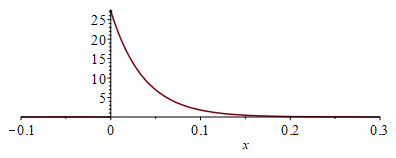

This is a continuous distribution that describes the time between independent events when the average time between events is $b$. So for example, if a call center receives 27.2 calls per hour, then the average time between calls must be $\frac{1}{27.2} \approx 0.03676470588$ hours or 2 minutes and 12 seconds; however, the time between any two events is not going to be exactly 2 minutes and 12 seconds. The exponential distribution describes the time intervals between such events.

[> X3 := RandomVariable( 'Exponential( delta )' ): [> Mean( X3 );

$\delta$

[> StandardDeviation( X3 );

$\delta$

We can ask Maple for the probability density function and the cummulative distribution functions:

[> PDF( X3 );

$\left \{ \begin{matrix} 0 & x < 0 \\ \frac{e^{-\frac{x}{\delta}}}{\delta} \end{matrix} \right.$

[> CDF( X3 );

$\left \{ \begin{matrix} 0 & x < 0 \\ 1 - e^{-\frac{x}{\delta}} \end{matrix} \right.$

[> X3f := RandomVariable( 'Exponential( 1/27.2 )' ): [> Mean( X3f );

$0.03676470588$

[> StandardDeviation( X3f );

$0.03676470587$

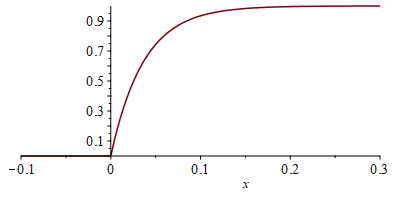

[> plot( PDF( X3f, x ), x = -0.1..0.3 );

[> plot( CDF( X3f, x ), x = -0.1..0.3 );

[> f3 := Sample( X3f ): [> f3( 10 );

$[0.008031484705298806, 0.030336664409757984, 0.013972451141163746,$ $0.054243172757515196, 0.018605132125918897, 0.03721196813390189,$ $0.04405742115148007, 0.0296437772133251, 0.032649770843399296,$ $0.009336955869392616]$